This week marks the first round of earnings reports. Companies expecting to report include Eaton (ETN), Merrill Lynch (MER), Coca-Cola (KO), Johnson & Johnson (JNJ), Intel (INTC), Yahoo (YHOO), Altria (MO), JP Morgan (JPM), eBay (EBAY), Google (GOOG), and Caterpillar (CAT). These reports will try to justify the great month that all of the major indices are having.

The only real earnings precursor came last week with reports from Alcoa (AA) and General Electric (GE). Both stocks boosted strong earnings results and investors responded nicely, but I am not entirely confident that the post-earnings rallies were due to the financial status of the firms. AA was down pre-market, but when an analyst suggested the buyout attractiveness of Alcoa, the ticker arrows quickly shifted direction.

GE had a really great report as well, but the total market was in the mist of a strong rally and GE may have simply rode the market wave last Friday.

Some final thoughts and a Bearish Warning:

Last season I suggested that investors would continue reacting well to earnings beats, even with the lowered yearly expectations. I am confident that if the beats continue, investors will once again ignore the lowered expectations and reward successful firms. I also predict that in-line reports will not be good enough to sustain the summer rally. A large part of this bullish run is unwarranted and not justified by earnings reports, leaving much of this month's run-ups susceptible for a pullback. I would encourage investors to wait a day or two and investigate the initial reports to better gauge the potential success for the rest of the earnings season.

Good luck all!

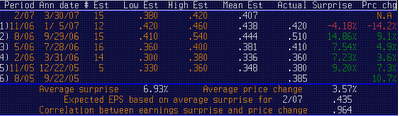

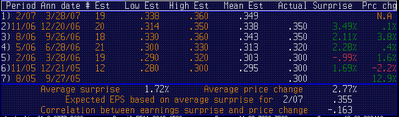

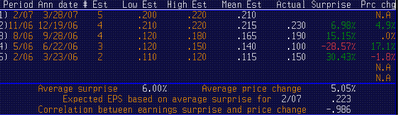

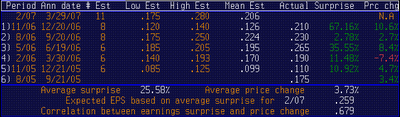

This is a good opportunity for investors to cash in on a potential upside catalyst. The recent sell-off has pushed the stock's P/E below the industry's average, reducing a lot of downside pressure on the stock if tomorrow's earnings go bad. Another nice thing about this play is the high correlation between the earning surprises and changes in the stock's price (around .964, with 1 being the highest). With this correlation investors do not have to worry about having a negative stock reaction after a positive release.

This is a good opportunity for investors to cash in on a potential upside catalyst. The recent sell-off has pushed the stock's P/E below the industry's average, reducing a lot of downside pressure on the stock if tomorrow's earnings go bad. Another nice thing about this play is the high correlation between the earning surprises and changes in the stock's price (around .964, with 1 being the highest). With this correlation investors do not have to worry about having a negative stock reaction after a positive release.