It has been a tough month for most investors as the DOW and S&P have fallen almost 2% each. Are there still buying opportunities, or is it time to sell and run? What fascinates me most about this recent sell-off is the significant pull back of large dividend stocks. PNG, PFE, and AEE all dish out more than a 4.5% dividend, but have fallen more than 4x the major indices. Intuitively, these stocks should not sell-off in this environment and buying these companies could quickly become a great hedge in an falling market.

So why are these great buys?

There are two main reasons why these are great buys. The first reason is the failed correlation between the major indices and dividend achievers. The ability for these companies to perform and adhere to their targeted profits has nothing to do with the movement of the DOW during the last couple of weeks. It is very likely that these companies will perform as promised and pay the expected dividend no matter what their investors want their shares to sell for. The second reason to buy is because of the pure increase in the value of the dividend yield with the recent decrease in share price. Dividend yield percentage and stock price share an inverse relationship; so as long as the price drops, the dividend yield grows. If the dividend payments are paid as promised, shareholders will get the same payout for cheaper!

So why did these stock sell-off then?

Predicted volatility showed his face again and scared shareholders. Analysts were big on dividend stocks early in the year when the market was fluctuating and investors had little certainty in the direction of the market. Dividend stocks became every investors go-to, causing these stocks to not only show dividend gains to investors, but capital gains with increased buying pressure. This month, major indices have sold off leaving these dividend holders a reason to take profit on their unwarranted share price gains.

So why are these great buys?

There are two main reasons why these are great buys. The first reason is the failed correlation between the major indices and dividend achievers. The ability for these companies to perform and adhere to their targeted profits has nothing to do with the movement of the DOW during the last couple of weeks. It is very likely that these companies will perform as promised and pay the expected dividend no matter what their investors want their shares to sell for. The second reason to buy is because of the pure increase in the value of the dividend yield with the recent decrease in share price. Dividend yield percentage and stock price share an inverse relationship; so as long as the price drops, the dividend yield grows. If the dividend payments are paid as promised, shareholders will get the same payout for cheaper!

So why did these stock sell-off then?

Predicted volatility showed his face again and scared shareholders. Analysts were big on dividend stocks early in the year when the market was fluctuating and investors had little certainty in the direction of the market. Dividend stocks became every investors go-to, causing these stocks to not only show dividend gains to investors, but capital gains with increased buying pressure. This month, major indices have sold off leaving these dividend holders a reason to take profit on their unwarranted share price gains.

I hope to share some of my favorite dividend buys later in the week.

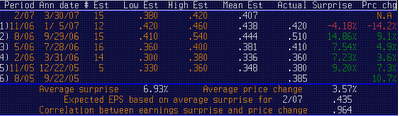

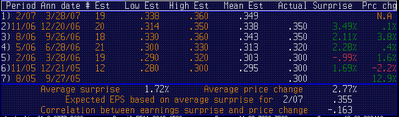

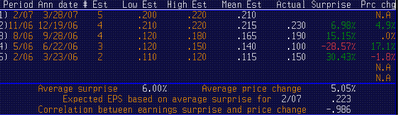

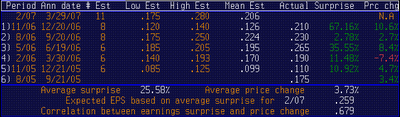

This is a good opportunity for investors to cash in on a potential upside catalyst. The recent sell-off has pushed the stock's P/E below the industry's average, reducing a lot of downside pressure on the stock if tomorrow's earnings go bad. Another nice thing about this play is the high correlation between the earning surprises and changes in the stock's price (around .964, with 1 being the highest). With this correlation investors do not have to worry about having a negative stock reaction after a positive release.

This is a good opportunity for investors to cash in on a potential upside catalyst. The recent sell-off has pushed the stock's P/E below the industry's average, reducing a lot of downside pressure on the stock if tomorrow's earnings go bad. Another nice thing about this play is the high correlation between the earning surprises and changes in the stock's price (around .964, with 1 being the highest). With this correlation investors do not have to worry about having a negative stock reaction after a positive release.